CleverAdviser

CleverAdviserWritten by Anthony Walters – Clever‘s Head of ESG & Christos Chountoulesis our Investment Analyst, the Market Review is packed with the most interesting and impactful events of the past week from the global financial markets.

Market Recap.

US markets suffered minor losses for the week with the Nasdaq 100 ETF (-1.42%), S&P 500 ETF (-1.84%), and Dow Jones ETF (-2.56%) all undoing gains from the prior week as markets priced in the expectation of higher interest rates. In the UK, the FTSE 100 ETF fell by 3.61% as the Bank of England reminded the market that inflation is still too high.

News.

Andrew Bailey, governor of the Bank of England, has warned the path of interest rates is likely to differ from the path expected by the market. “I have always been interested that markets think that the peak will be short lived in a world [where] we are dealing with more persistent inflation,” he said. However, Bailey did say he thought rates will “have to go up by less than currently priced in financial markets”.

Geopolitics.

U.S. Treasury Secretary Janet Yellen urged closer communication between China and the United States to improve economic decision-making. Despite bilateral tensions, record high U.S.-Chinese trade last year showed there was “ample room” to engage in trade and investment, and it was critical to focus on areas of common interest.

Inflation.

European Central Bank President Christine Lagarde said the bank will not “stand idly by” if there is a simultaneous increase in profits and wages, given persistently high inflation in the region. Lagarde said it was important to know whether companies plan to reduce their margins, “which is what has normally happened during previous high inflation episodes, or whether we are going to see a twofold increase, in margins and in wages”.

Central Banks.

Nearly all policymakers at the Federal Reserve’s June meeting believed it was appropriate to hold the bank’s benchmark interest rate steady, but investors should still expect borrowing costs to rise this year. Federal Reserve policymakers still predict a mild and short recession likely will hit the U.S. later this year.

Commodities.

Energy-powered commodity returns for the week with, Coal (9.19%), Heating Oil (4.39%), WTI Crude Oil (2.66%) and Brent Crude Oil (2.40%) leading the way. In paradoxical fashion, Ethanol and Natural gas declined, with a loss of 7.74% and 6.97% respectively.

ESG.

Nestlé will shift away from the use of offsets to achieve carbon neutral brands, focusing instead on actual emissions reductions in its operations and value chain, according to a company spokesperson, following media reports that the company was walking away from carbon neutral pledges for some brands.

Week Ahead.

In the UK, the final estimate of first quarter GDP, monetary indicators, and nationwide housing price data will be published. Europe will publish preliminary inflation rates for the Eurozone, which is expected to fall. The ECB Forum on Central Banking in Portugal will gather central bank governors, including Lagarde and Jerome Powell, to discuss macroeconomic stabilisation amid volatile inflation.

Deep Dive

UK economy – Inflation and its effect on growth and the housing market.

On 30th June 2023, data confirmed that UK GDP achieved an annual growth rate of 0.2% regarding Q1 2023 (on a year-on-year basis). However, this has been the weakest expansion for the UK economy in the last two years as per the bar chart below:

UK GDP Annual Growth Rate

Source: Trading Economics – July 2023

This anemic GDP growth rate can be attributed to lower overall economic activity and demand, caused by high inflation. The latter, despite showing signs of easing, remained stubbornly high at 8.7% for June 2023 as per the bar chart below:

UK Consumer Price Index

Source: Trading Economics – July 2023

To tackle inflation, Bank of England has now increased interest rates 13 times in a row, with its latest decision in June 2023 resulting in an interest rate of 5.0%, the highest since the 2008 financial crisis.

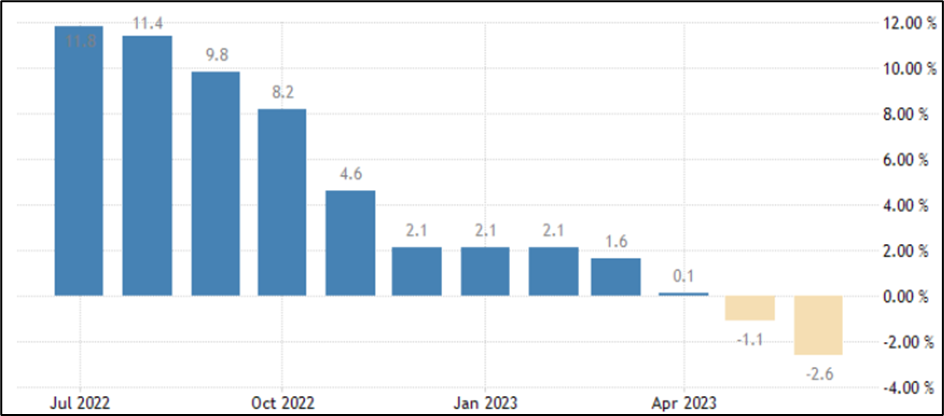

The combination of increased borrowing costs and higher inflation has placed a squeeze on household finances, which is reflected in the housing market. Borrowers on fixed-term mortgages due for refinancing and those looking to get into the property ladder by getting a mortgage are both facing the prospect of higher monthly mortgage repayments than last year, dampening demand. The effect can be seen in the house prices, which have been decreasing since May 2023, after months of slow increases. Available data as on 7th July 2023 indicate that the Halifax House Price index shown below fell by 2.6% (on a year-on-year basis) in June 2023, following a reduction of 1.1% in house prices the previous month.

Halifax House Price Index

Source: Trading Economics – July 2023

It is probably too early to assess the full impact of high inflation on the housing market or the economy. In relation to the housing market though, the stickier inflation proves, the higher the interest rate in the UK is poised to remain (and for longer), which will keep borrowing costs higher and decrease demand for house purchases, which will push house prices lower. New inflation data are expected later in July 2023, for which the market currently forecasts a lower rate of inflation of 8.3%, reduced by 0.4% compared to June 2023.

Sources:

Anthony Walters – Head of ESG, Christos Chountoulesis – Investment Analyst at Clever Adviser Technology Ltd (Clever)

Market recap – Data sourced from FE FundInfo & Koyfin. ETFs quoted: iShares Core FTSE 100 UCITS ETF, iShares Core S&P 500 UCITS ETF, iShares Nasdaq 100 UCITS ETF.

News – BoE governor Bailey: Rates will likely stay higher for longer by Elliot Gulliver-Needham, Investment Week

Inflation – ‘We would not stand idly by’: Lagarde pledges ECB action if both profits and wages rise, by Silvia Amaro, CNBC 07/07/23

Central Banks – ‘Almost All’ Fed Officials Opted for June Rate Pause. A July Increase Is on the Table by Megan Leonhardt, Barrons, 05/07/23

ESG – Nestlé Moves Away from Carbon Offsets to Focus on Emissions Reductions Across Brands by Mark Segal, ESG Today, 03/07/23

Geopolitics – Yellen urges US-China cooperation on economy, climate By Andrea Shalal, Reuters, 08/07/23

Commodities – Data sourced from Koyfin and Investing.com

Week ahead – Data sourced from Investing.comRisk Warning: These are Nathan’s views at the time of writing and should not be construed as investment advice. The opinions expressed are correct at time of writing and may be subject to change. Capital is at risk. The value and income from investments can go down as well as up and are not guaranteed. An investor may get back significantly less than they invest. Past performance is not a reliable indicator of current or future performance and should not be the sole factor considered when selecting funds.

Regulatory Information: This is a general communication provided for informational purposes only. It is educational in nature and not designed to be taken as advice or a recommendation for any specific investment product, strategy, plan feature or other purpose in any jurisdiction, nor is it a commitment from Marlborough or any of its subsidiaries to participate in any of the transactions mentioned herein. Any examples used are generic, hypothetical and for illustration purposes only. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any securities or products. In addition, users should make an independent assessment of the legal, regulatory, tax, credit, and accounting implications and determine – together with their own professional advisers if appropriate – if any investment mentioned herein is believed to be suitable. Investors should ensure that they obtain all available relevant information before making any investment. Any forecasts, figures, opinions or investment techniques and strategies set out are for information purposes only, based on certain assumptions and current market conditions and are subject to change without prior notice.

All information presented herein is considered to be accurate at the time of production, but no warranty of accuracy is given and no liability in respect of any error or omission is accepted. Issued by Marlborough Investment Management Limited, authorised and regulated by the Financial Conduct Authority (reference number 115231). Registered office: PO BOX 1852 Lichfield, Staffordshire, England, WS13 8XU. Registered in England No. 01947598. The Clever Marlborough Model Portfolio Service (‘Clever MPS’) is a collaboration between Marlborough Investment Management Limited as the Discretionary Fund Manager and Clever Adviser Technology Limited, a company registered in England and Wales (company number 2910523) with registered office at Watergate House, 85 Watergate Street, Chester, Cheshire CH1 2LF (“Clever”). Clever is a technology and software provision company which developed a methodology and proprietary suite of algorithms for the monitoring, analysis, collation, and transmission of data on the performance of Investment Funds and related portfolios within the UK market which Marlborough utilises for investment purposes.